Summary

The BCG Matrix for Banking Industry helps evaluate how banks allocate resources across various financial services such as retail banking, corporate lending, wealth management, digital banking, and insurance. In an era where digital transformation, regulatory changes, and customer expectations are redefining banking, understanding the BCG Matrix offers critical insights into strategic growth and profitability.

This comprehensive guide explains how the BCG Matrix in banking sector categorizes different banking services into Stars, Cash Cows, Question Marks, and Dogs, helping financial institutions prioritize investment, manage risk, and maintain competitiveness in an evolving global market.

The global banking industry is undergoing a rapid transformation driven by technology, competition, and customer-centric innovation. Traditional banking models are evolving, with digital services, fintech partnerships, and sustainability goals reshaping how banks operate. To navigate this complexity, financial institutions use strategic tools like the BCG Matrix to evaluate performance and allocate resources effectively.

The BCG Matrix for Banking Industry (Boston Consulting Group Matrix) provides a framework that classifies banking services based on market growth and market share. It helps identify which services are performing well, which need further investment, and which may require restructuring or phasing out.

By applying this model, banks can ensure an optimal balance between profitability, innovation, and risk management.

What is the Banking Industry Landscape

Before applying the BCG Matrix in the banking sector, it’s important to understand the key characteristics of modern banking:

- Customer-Centric Approach: Banks now focus on personalized services and digital convenience.

- Technological Transformation: AI, blockchain, and digital platforms are redefining how banks operate.

- Intense Competition: Private banks, government institutions, and fintech startups compete for market dominance.

- Regulatory Oversight: Compliance and risk management remain critical for long-term stability.

- Diversified Offerings: Banks operate across retail, corporate, SME, wealth, and digital banking segments.

In such a multifaceted industry, the BCG Matrix for banks provides clarity on which business units should receive priority and which should be optimized.

What is the BCG Matrix?

The Boston Consulting Group (BCG) Matrix is a portfolio analysis tool that evaluates business units or services based on:

- Market Growth Rate (vertical axis)

- Relative Market Share (horizontal axis)

It divides a company’s business units into four categories:

- Stars (High Growth, High Market Share)

- Cash Cows (Low Growth, High Market Share)

- Question Marks (High Growth, Low Market Share)

- Dogs (Low Growth, Low Market Share)

When applied to banking, this model helps classify different services such as digital banking, retail lending, or investment services, providing actionable insights into resource allocation and strategic planning.

Why the BCG Matrix Matters for Banks

The BCG Matrix for the Banking Industry is not just a theoretical model—it’s a practical framework that guides how banks manage their product and service portfolios. Here’s why it’s critical:

Strategic Resource Allocation

Banks operate multiple business lines simultaneously. The BCG Matrix helps management determine which divisions deserve more investment (Stars), which can be maintained for steady returns (Cash Cows), and which should be divested (Dogs).

Improved Decision-Making

By quantifying performance, the BCG Matrix in banking sector provides an evidence-based approach for top-level decision-making, minimizing bias and maximizing profitability.

Balancing Growth and Stability

Banks need both innovation and consistency. The Matrix ensures a healthy balance by allowing stable divisions to fund growth-oriented projects.

Managing Risk in a Volatile Market

In an industry exposed to interest rate fluctuations and regulatory constraints, the BCG Matrix helps identify underperforming units early, reducing financial risk.

Applying the BCG Matrix to the Banking Industry

Let’s analyze how major banking services can be positioned within the BCG Matrix for Banking Industry.

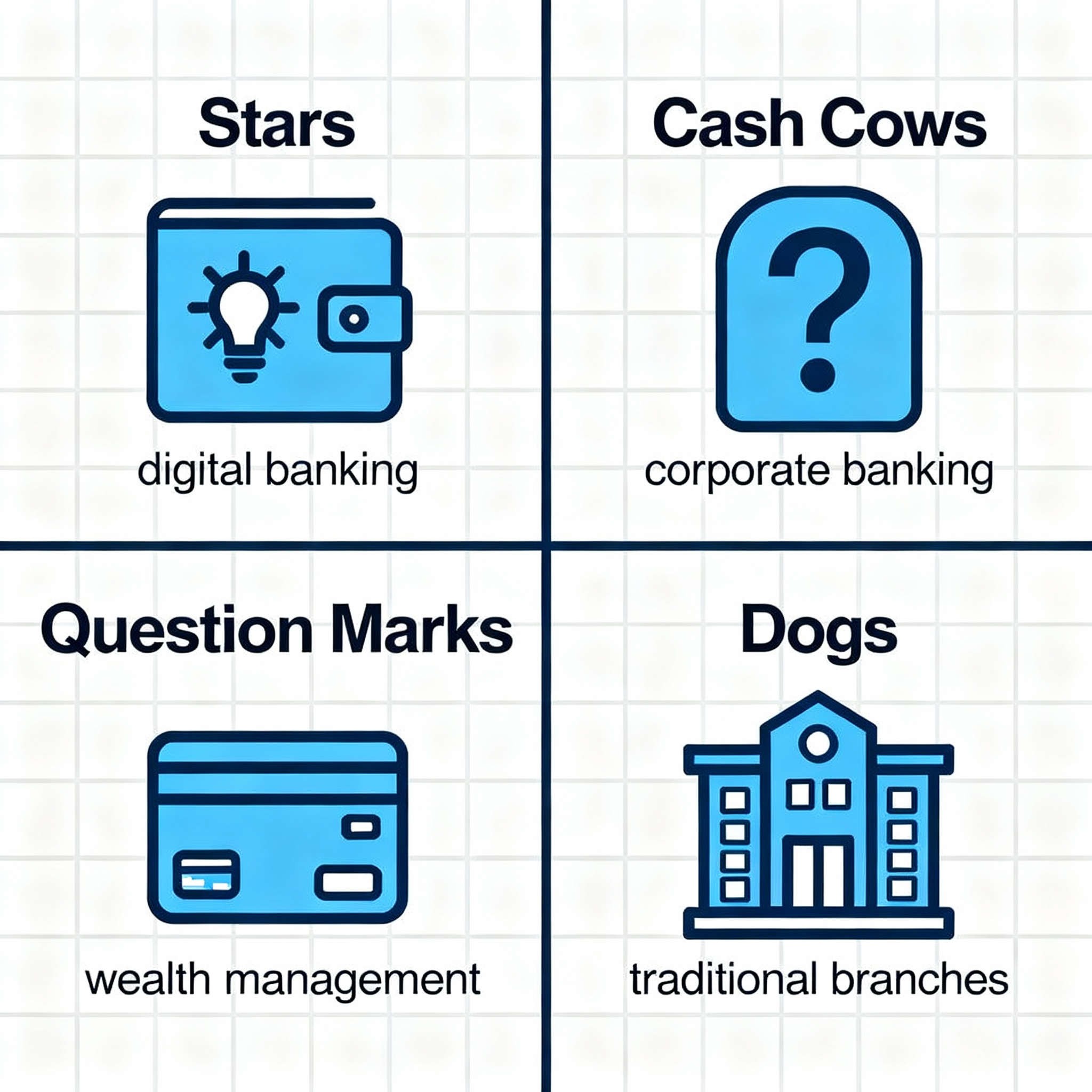

Stars (High Market Share, High Market Growth)

Stars are high-performing business areas in a rapidly growing market. These divisions demand significant investment but also generate strong returns.

Digital Banking

- Overview: The digital revolution has transformed how customers interact with banks. Services like mobile banking, digital payments, and online loans are experiencing exponential growth.

- Why it’s a Star: Digital banking has high customer adoption and rapid innovation cycles. Banks that invest in technology and AI see improved operational efficiency and customer satisfaction.

- Example: HDFC Bank’s “Digital 2.0” initiative and Axis Bank’s “Open by Axis” platform are perfect examples of Stars in this category.

Corporate Banking

- Overview: Serving large corporates with working capital, trade finance, and investment banking solutions.

- Why it’s a Star: With globalization and mergers on the rise, corporate banking continues to grow steadily. Banks offering digital trade services and cross-border payment platforms are leading the market.

Conclusion: Stars like digital and corporate banking represent the growth engine of modern banks and need continuous innovation and investment.

Cash Cows (High Market Share, Low Market Growth)

Cash Cows are mature business units that consistently generate revenue with minimal investment.

Retail Banking

- Overview: Includes savings accounts, personal loans, fixed deposits, and mortgages.

- Why it’s a Cash Cow: This segment offers stable income and loyal customers, even though market growth is modest.

- Example: SBI, ICICI, and HDFC Bank derive substantial profits from retail operations.

Credit Cards & Loan Portfolios

- Overview: Despite fierce competition, credit card services and loan portfolios remain strong revenue contributors.

- Why it’s a Cash Cow: Customers’ recurring credit use and high interest margins keep this division profitable.

Conclusion: Cash Cow segments provide the financial foundation that supports innovation in high-growth areas like digital transformation.

Question Marks (Low Market Share, High Market Growth)

These are emerging sectors with potential but currently low market share. They require strategic investment and analysis to determine future viability.

Wealth Management and Insurance

- Overview: Rising disposable income and financial awareness have fueled demand for wealth management and insurance products.

- Why it’s a Question Mark: Although the sector is expanding rapidly, competition from fintech firms and mutual fund companies limits banks’ dominance.

- Future Outlook: With technological integration and advisory-driven models, this sector could become a Star in the next few years.

Sustainable and Green Banking

- Overview: As ESG (Environmental, Social, Governance) principles gain traction, banks are offering green finance and sustainability-linked loans.

- Why it’s a Question Mark: The concept is still new in developing economies but expected to grow with regulatory support.

- Future Outlook: With climate financing becoming a global priority, this area can transition into a Star.

Conclusion: Question Marks are experimental divisions that could become future profit drivers with the right investments and strategic focus.

Dogs (Low Market Share, Low Market Growth)

Dogs are divisions that generate minimal returns and have limited growth potential.

Also Read: Parle BCG Matrix

Traditional Branch Banking

- Overview: Physical branches, though essential, are seeing declining relevance due to digital adoption.

- Why it’s a Dog: High operational costs and reduced footfall make traditional branches less profitable.

- Strategy: Banks are now converting physical branches into digital kiosks or advisory hubs to optimize costs.

Legacy Lending Operations

- Overview: Older loan schemes or unprofitable lending models that haven’t adapted to new market conditions.

- Why it’s a Dog: Increasing NPAs (Non-Performing Assets) and regulatory pressure make these operations risky.

- Strategy: Banks should streamline or integrate such models into more efficient frameworks.

Conclusion: Dogs require cost rationalization or strategic divestment to improve overall profitability.

BCG Matrix Diagram for the Banking Industry

| Quadrant | Banking Services | Market Growth | Market Share | Strategy |

| Stars | Digital Banking, Corporate Banking | High | High | Invest and Innovate |

| Cash Cows | Retail Banking, Credit Cards | Low | High | Maintain and Harvest |

| Question Marks | Wealth Management, Green Banking | High | Low | Selective Investment |

| Dogs | Traditional Branch Banking, Legacy Lending | Low | Low | Optimize or Exit |

Strategic Insights from the BCG Matrix in Banking

- Digital Transformation Is the Future: Digital and mobile banking dominate the Star quadrant, showing how technology reshapes profitability.

- Retail Banking Remains the Backbone: Despite slow growth, retail banking continues to provide steady profits.

- Investment in Emerging Sectors Is Essential: Green finance and wealth management present immense future opportunities.

- Optimization of Legacy Systems: Reducing dependency on low-growth, high-cost divisions helps improve efficiency.

- Balanced Growth Approach: A well-structured portfolio ensures both immediate returns and long-term sustainability.

Benefits of BCG Matrix in the Banking Sector

- Portfolio Optimization: Helps banks maintain a balanced mix of high-growth and stable services.

- Resource Prioritization: Guides capital allocation toward high-potential sectors.

- Performance Evaluation: Enables quantitative analysis of profitability across business divisions.

- Strategic Planning: Supports decision-making for mergers, acquisitions, or divestments.

- Innovation Focus: Encourages banks to invest in technology and sustainability-driven initiatives.

Challenges and Limitations of BCG Matrix for Banks

While highly effective, the BCG Matrix for banking industry has certain limitations:

- Interconnected Services: Many banking divisions overlap, making clear classification difficult.

- Dynamic Market Factors: Regulatory policies, inflation, and interest rate changes can rapidly shift growth rates.

- Non-Quantifiable Metrics: Factors like customer trust and brand value are not captured in the matrix.

- Short-Term Focus: The matrix emphasizes current market conditions, not long-term potential.

Therefore, banks often use the BCG Matrix alongside tools like SWOT Analysis, PESTEL Analysis, and Ansoff Matrix for comprehensive strategic planning.

Conclusion

The BCG Matrix for Banking Industry provides a powerful framework for understanding how financial institutions manage diverse business units in a rapidly changing environment.

- Stars: Digital and Corporate Banking drive innovation and market growth.

- Cash Cows: Retail and credit services provide stable income.

- Question Marks: Wealth management and green finance hold future promise.

- Dogs: Traditional operations require restructuring or automation.

By strategically leveraging this model, banks can allocate resources effectively, innovate intelligently, and sustain profitability in the long run. The banking BCG analysis proves that adaptability, technology, and customer-centricity are key to long-term success in the modern financial landscape.

FAQs

Q1. What is the BCG Matrix for Banking Industry?

The BCG Matrix for Banking Industry categorizes banking services into Stars, Cash Cows, Question Marks, and Dogs based on market growth and market share to guide investment and resource allocation.

Q2. Which banking services are considered Stars?

Digital Banking and Corporate Banking are Stars due to their high growth and dominant market share.

Q3. What are Cash Cows in the banking sector?

Retail Banking and Credit Card services are Cash Cows, generating consistent profits despite slower growth.

Q4. Why is Digital Banking considered crucial in the BCG analysis?

Digital Banking is a Star because it offers scalability, innovation, and strong customer engagement in a fast-growing market.

Q5. What is the role of Question Marks in the BCG Matrix for banks?

Question Marks like Wealth Management and Green Banking represent future opportunities that need investment to become profitable.

A digital marketer with a strong focus on SEO, content creation, and AI tools. Creates helpful, easy-to-understand content that connects with readers and ranks well on search engines. Loves using smart tools to save time, improve content quality, and grow online reach.