Summary

Bank of Baroda (BoB), one of India’s leading public sector banks, has grown into a global institution with a network spanning 17 countries. Founded in 1908, it has successfully combined legacy trust with digital innovation through initiatives like the bob World app. This SWOT analysis of Bank of Baroda highlights the bank’s major strengths, weaknesses, opportunities, and threats in 2025.

From its massive branch network and strong government backing to challenges like NPAs, digital competition, and operational inefficiencies, the analysis of Bank of Baroda provides insights into how the bank can remain competitive in India’s fast-changing financial sector.

Bank of Baroda, often called “India’s International Bank,” has been a cornerstone of Indian banking for over a century. Established by Maharaja Sayajirao Gaekwad III of Baroda in 1908, the bank has steadily expanded domestically and internationally. After its merger with Vijaya Bank and Dena Bank in 2019, it became the third-largest lender in India, further strengthening its footprint.

In 2025, with a customer base of more than 165 million and operations in 17 countries, the swot analysis of Bank of Baroda provides clarity on where the bank stands today and how it can adapt to upcoming challenges.

Overview of Bank of Baroda

- Industry: Banking, Financial Services

- Predecessors: Vijaya Bank, Dena Bank (merged in 2019)

- Founded: July 20, 1908

- Founder: Sayajirao Gaekwad III

- Headquarters: Vadodara, Gujarat, India

- Global Reach: 8,243 branches, 10,000+ ATMs, 91 overseas offices across 17 countries

- Key People: Hasmukh Adhia (Chairman), Debadatta Chand (MD & CEO)

- Revenue (2024): ₹1.42 lakh crore (US$17 billion)

- Operating Income (2024): ₹25,799 crore (US$3.1 billion)

- Net Income (2024): ₹18,767 crore (US$2.2 billion)

- Total Assets (2024): ₹16.55 lakh crore (US$200 billion)

- Ownership: Government of India – 63.97% stake

- Employees: ~79,806 (2022)

- Website: www.bankofbaroda.in

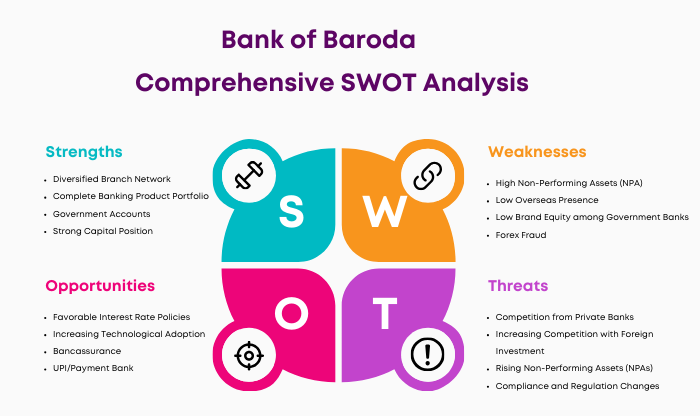

SWOT Analysis of Bank of Baroda (2025)

Strengths of Bank of Baroda

- Diversified Branch Network

With over 8,243 branches and 91 overseas offices, Bank of Baroda has a strong domestic and international presence. Its network reduces dependency on high-cost deposits and provides access to a wider customer base. This reach also supports cross-border trade finance and remittance services. - Comprehensive Product Portfolio

The bank offers a one-stop solution for retail, corporate, SME, and rural banking. From savings accounts to wealth management, BoB ensures that all customer segments are covered under one umbrella. - Government Accounts and Trust

Being a public sector bank, BoB handles several government accounts, including pensions and salaries. This association ensures a stable and loyal customer base, particularly among government employees and retirees. - Strong Capital Position

With deposits of over ₹13.26 lakh crore and advances of ₹10.89 lakh crore (2024), BoB maintains a strong balance sheet. Its capital adequacy ratio (CAR) of 37.81% highlights its financial stability. - Second Largest Bank in India

Bank of Baroda is India’s second-largest public sector bank after SBI, with a market cap exceeding $17 billion. Its scale strengthens its ability to compete with both private and foreign banks. - Large Customer Base

BoB serves 165 million customers globally, supported by over 70,000 touchpoints. This vast customer base enhances revenue diversification and cross-selling opportunities. - Merger Synergies

The merger with Vijaya Bank and Dena Bank enhanced operational efficiency, increased branch coverage, and widened the client base. It also improved economies of scale and reduced duplication of services. - Competitive Interest Rates

Compared to private banks, BoB offers lower loan interest rates, making it attractive to cost-sensitive customers in retail and SME segments. - Established Brand

With over a century of trust, Bank of Baroda has a strong brand reputation. Generations of Indians recognize it as a reliable financial partner. - International Presence

Operations across 17 countries diversify risks and provide opportunities in global markets, especially among the Indian diaspora. - Digital Advancements

The bob World app records over 8 million daily transactions, showcasing BoB’s shift toward digital banking. Its focus on mobile-first services caters to tech-savvy customers. - Training and HR Infrastructure

BoB invests heavily in training, ensuring its workforce is updated with modern banking practices, customer service skills, and compliance knowledge. - Experienced Management Team

Leadership with decades of industry experience ensures strategic decision-making and resilience in volatile markets. - CSR and Financial Inclusion

Through financial literacy programs, rural banking, and CSR projects, BoB strengthens its community engagement and fulfills its role as a socially responsible bank. - Risk Management Practices

BoB’s robust risk frameworks help mitigate credit, operational, and market risks, ensuring long-term stability.

Weaknesses of Bank of Baroda

- High Non-Performing Assets (NPAs)

NPAs remain a major challenge, eating into profits and damaging investor confidence. Managing asset quality is crucial for sustainable growth. - Limited Global Revenue Contribution

Despite 91 international offices, most revenues are generated in India, making BoB vulnerable to domestic economic slowdowns. - Low Brand Equity Among Younger Customers

Compared to private banks with aggressive marketing, BoB’s image is perceived as traditional, reducing its appeal to millennials and Gen Z. - Past Regulatory Issues

Incidents like the ₹6,000 crore forex scam damaged the bank’s reputation and highlighted compliance challenges. - Integration Challenges Post-Merger

The merger created overlapping branches and cultural differences among staff, affecting operational efficiency. - Operational Inefficiencies

Decision-making can be slow in large PSUs, limiting agility in responding to fintech disruption. - Lag in Digital Transition

Though improving, BoB still trails behind private banks in digital experience and innovation. - Employee Productivity Issues

PSU work culture sometimes impacts efficiency, customer service consistency, and staff motivation. - Over-Reliance on Traditional Banking

Heavy dependence on loans and deposits restricts diversification into fee-based income like wealth management. - Aging Infrastructure

Many branches still operate on outdated infrastructure, which can impact service delivery and brand image.

Opportunities for Bank of Baroda

- Rising Interest Rates

RBI’s monetary policy changes create opportunities to improve net interest margins and profitability. - Technological Adoption

Increased digital adoption in India allows BoB to strengthen bob World, UPI, and online services for cost efficiency and wider reach. - Bancassurance Expansion

With its joint venture in IndiaFirst Life Insurance, BoB can cross-sell insurance products and grow fee-based income. - UPI and Payment Ecosystems

By innovating in UPI apps and digital wallets, BoB can capture India’s booming payment market. - Infrastructure and Loan Market Growth

India’s infrastructure push creates demand for large project financing, which BoB is well-positioned to provide. - SME and MSME Lending

These sectors are the backbone of India’s economy. Tailored lending products can deepen relationships and revenue. - Rural Banking Opportunities

Expanding into underbanked rural areas can enhance financial inclusion and create long-term loyal customers. - International Expansion

Entering new overseas markets or strengthening current ones can diversify risks and boost revenues. - Collaborations with Fintechs

Partnerships with fintechs can enhance customer experience, improve analytics, and speed up innovation. - Green and Sustainable Finance

Financing renewable energy projects and offering green banking products aligns with global ESG trends. - Mutual Funds and Wealth Management

With rising disposable income, there is growing demand for investment products that BoB can capitalize on. - Government Initiatives

By participating in schemes like PMJDY and affordable housing, BoB can expand its reach and social impact.

Threats to Bank of Baroda

- Private Bank Competition

Aggressive marketing and digital-first services from private banks like HDFC and ICICI erode BoB’s market share. - Foreign Investment Competition

With foreign banks allowed to invest up to 74%, competition in the Indian banking sector is intensifying. - Rising NPAs

Continued defaults can affect profitability, requiring tighter credit monitoring. - Regulatory Changes

Shifts in RBI or government policies can force costly adjustments. - Economic Slowdowns

Reduced borrowing and spending during downturns increase stress on profitability. - Fintech Disruption

Startups and digital-only banks attract tech-savvy customers with innovative solutions. - Cybersecurity Risks

With digital adoption rising, cyber threats pose reputational and financial risks. - Interest Rate Volatility

Sudden changes in interest rates can impact treasury operations and loan growth. - Reputation Risks

Any future scandals or compliance lapses could hurt BoB’s century-old reputation. - Geopolitical Tensions

Overseas operations face risks from international instability.

Conclusion

The SWOT analysis of Bank of Baroda reveals a bank with immense strengths: scale, government trust, and a global presence. However, challenges like NPAs, digital transition gaps, and operational inefficiencies need urgent attention.

Opportunities in digital banking, SME lending, wealth management, and green finance are promising. But threats from fintechs, private banks, and economic volatility must be managed with innovation and resilience.

Bank of Baroda’s long-term growth will depend on balancing its historic strengths with bold modernization strategies in 2025 and beyond.

FAQs

Why is Bank of Baroda important in India’s banking sector?

It is India’s second-largest public sector bank with global reach and a 115-year legacy.

What are Bank of Baroda’s biggest strengths?

Its large branch network, strong government trust, digital innovations, and wide product portfolio.

What are the key weaknesses of Bank of Baroda?

High NPAs, slower digital transition, operational inefficiencies, and lower brand appeal among younger customers.

What opportunities exist for Bank of Baroda in 2025?

Digital banking expansion, rural inclusion, green finance, fintech partnerships, and SME lending.

What threats does Bank of Baroda face?

Intense competition from private banks and fintechs, cybersecurity risks, regulatory changes, and rising NPAs.

How did the Vijaya and Dena Bank merger impact BoB?

It created India’s third-largest lender, expanded customer reach, and improved efficiency, though integration challenges remain.

Is Bank of Baroda focusing on digital banking?

Yes, through initiatives like the bob World app, which records millions of daily transactions.

A digital marketer with a strong focus on SEO, content creation, and AI tools. Creates helpful, easy-to-understand content that connects with readers and ranks well on search engines. Loves using smart tools to save time, improve content quality, and grow online reach.