Summary

HDFC Bank, one of India’s most trusted financial institutions, has grown into a global banking powerhouse with a stronghold in retail, corporate, and digital banking. This blog explores a detailed SWOT analysis of HDFC Bank, covering its strengths, weaknesses, opportunities, and threats in 2025. From its vast branch network and leadership in payment technologies to challenges like limited rural penetration and rising fintech competition, this analysis of HDFC Bank highlights where it excels and where it must adapt.

Since its foundation in 1977, Housing Development Finance Corporation Limited (HDFC) has transformed into a financial giant. It started as a pioneer in housing finance and gradually diversified into banking, insurance, asset management, and digital services. Today, HDFC Bank is India’s largest private-sector bank by assets and a recognized leader in retail and digital banking.

The SWOT analysis of HDFC Bank provides valuable insights into its current market standing, areas for improvement, growth opportunities, and external threats in 2025. Understanding this helps investors, students, and professionals evaluate the analysis of HDFC Bank more effectively.

Overview of HDFC

- Company type: Public

- Industry: Financial services (banking, insurance, asset management, housing finance)

- Founded: August 1994 (HDFC Bank), while HDFC Ltd. was founded in 1977

- Headquarters: Mumbai, Maharashtra, India

- Key People: Atanu Chakraborty (Chairman), Sashidhar Jagdishan (CEO)

- Employees: 213,527 (2024)

- Website: www.hdfcbank.com

With the merger of HDFC Ltd. and HDFC Bank in 2023, the combined entity has become even stronger, blending housing finance dominance with India’s leading private bank.

SWOT Analysis of HDFC Bank (2025)

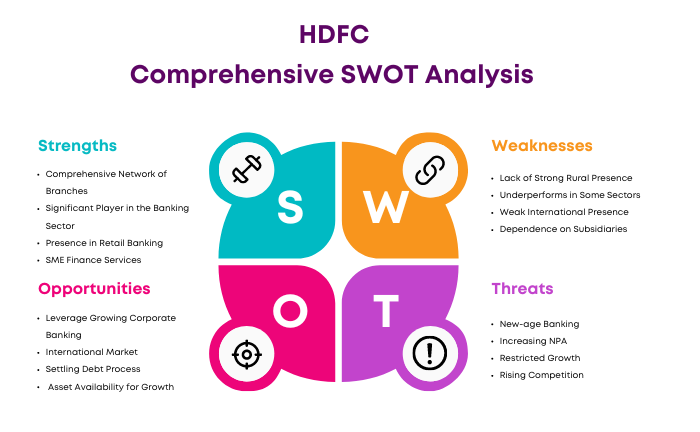

Strengths of HDFC Bank

- Comprehensive Network of Branches

HDFC Bank has built one of the most extensive branch and ATM networks in India, with 8,738 branches and 20,938 ATMs. This ensures accessibility for urban and semi-urban customers while reinforcing its stronghold in retail banking. The network enhances customer trust, convenience, and inclusivity. - Significant Player in the Banking Sector

HDFC Bank is India’s largest private bank by assets and the 4th largest globally by market capitalization, valued at over ₹11.13 trillion. This scale reflects investor trust, operational efficiency, and market dominance, making it a benchmark in the Indian financial services sector. - Strong Retail Banking Presence

The bank dominates retail banking through savings accounts, credit cards, personal loans, and consumer finance. In 2023 alone, retail loans grew by an impressive 108.9%, proving the bank’s stronghold in serving India’s middle-class and urban populations. - SME Finance Services

Small and Medium Enterprises (SMEs) are the backbone of India’s economy. HDFC Bank has introduced customized loans, trade finance, and credit solutions for SMEs, contributing to financial inclusion and supporting entrepreneurship. - High Customer Satisfaction

Customer loyalty and satisfaction are key differentiators. HDFC Bank’s Net Promoter Score grew 22% year-on-year, demonstrating its commitment to delivering value-driven banking experiences. - Leadership in Payment Technologies

With over 63 million payment cards in circulation, HDFC Bank controls one-third of India’s total card spending. Its leadership in card issuance and acceptance highlights its dominance in digital payments and fintech innovation. - Awards that Boost Reputation

HDFC Bank has consistently been recognized as “Best Bank” by Financial Express, Finance Asia, and several rating agencies. Awards validate its operational excellence and enhance customer confidence. - High Employee Retention Rate

The bank boasts an 83% retention rate, significantly higher than the industry average. This indicates strong company culture, reduced hiring costs, and continuity in customer relationships. - Merger with Parent HDFC

The strategic merger with HDFC Ltd. has strengthened the home loan portfolio, boosted cross-selling opportunities, and created India’s largest financial services powerhouse. - Technology-Driven Banking

HDFC Bank invests heavily in technology. With NetBanking, OTP-based security, and advanced mobile banking platforms, the bank reduces reliance on physical branches while improving customer convenience and cybersecurity.

Weaknesses of HDFC Bank

- Weak Rural Penetration

With only 1,415 rural branches, HDFC Bank lags behind competitors like SBI and ICICI in rural banking. This underutilizes India’s vast rural market potential. - Underperformance in Certain Sectors

Despite overall success, HDFC Bank has struggled with periodic underperformance. For instance, its profits in Q4 FY22 fell short of expectations, raising investor concerns about sector-specific strategies. - Minimal International Presence

Only 1.2% of HDFC Bank’s revenue comes from overseas markets. Heavy reliance on India makes the bank vulnerable to domestic economic slowdowns. - Overdependence on Subsidiaries

Subsidiaries like HDFC Life and HDFC Ltd. contribute significantly to overall performance. Any issues in these entities can directly impact the parent bank’s valuation and profitability. - Restrained Marketing Approach

Unlike ICICI Bank’s aggressive marketing, HDFC follows a more conservative branding strategy. This can make it seem “exclusive” and less accessible to lower-income customers. - Investor Uncertainty

Stock price volatility, especially after weaker earnings announcements, creates unease among investors despite the bank’s strong fundamentals. - Concentration Risk

Heavy reliance on retail banking, compared to a smaller corporate portfolio, increases the risk of sectoral downturns. - Loan Portfolio Vulnerability

Although diverse, HDFC Bank’s loan portfolio has concentration risks in certain industries. A downturn in these sectors could disproportionately impact its asset quality.

Opportunities for HDFC Bank

- Growth in Corporate Banking

With India’s economy growing, corporate credit demand is set to rise at double-digit levels. HDFC Bank has the infrastructure and brand trust to tap into this lucrative segment. - Expansion into International Markets

Globalization offers untapped opportunities. Expanding its footprint beyond India would diversify risks and strengthen HDFC’s global presence. - Better Debt Settlement Processes

Improving NPA resolution mechanisms can lead to faster recoveries, reduced defaults, and enhanced profitability. - Leverage Strong Asset Base

With high-quality assets, HDFC Bank is well-positioned to fund growth and maintain strong credit ratings. - Digital Transformation

Initiatives like Digital Factory, Enterprise Factory, and Enterprise IT empower HDFC Bank to stay ahead in fintech innovations and meet the rising demand for digital-first services. - Wealth Management Services

India’s affluent middle class is seeking more investment and wealth management solutions. HDFC can expand advisory services, portfolio management, and personalized investments. - Cross-Selling and Upselling

With a large base of existing customers, HDFC can increase revenue by selling complementary products like insurance, investment services, or premium credit cards.

Threats to HDFC Bank

- Rise of New-age Banking

Fintechs, digital wallets, and cryptocurrency platforms challenge traditional banks by offering faster, cheaper services. HDFC must innovate rapidly to stay competitive. - Increasing NPAs

NPAs have risen from 0.20% to 0.33%, signaling higher loan defaults. Even small increases can impact investor confidence and profitability. - Restricted Growth due to Competition

Aggressive marketing by ICICI Bank and SBI makes it difficult for HDFC to expand its market share. - Intensifying Competition from Fintechs & NBFCs

Startups and NBFCs are offering innovative, tech-driven financial services at lower costs, forcing HDFC to innovate constantly. - Cybersecurity Risks

As banking goes digital, cybersecurity threats loom large. Any breach could damage trust and invite heavy regulatory penalties. - Cryptocurrency Disruption

The popularity of cryptocurrencies creates challenges for traditional banking. HDFC must decide whether to integrate blockchain or risk being sidelined. - Capital Adequacy Requirements

Strict RBI norms require HDFC Bank to maintain strong capital reserves. Falling short may impact growth strategies. - Foreign Exchange Volatility

Fluctuations in global markets and foreign exchange can impact revenues, especially as HDFC scales international operations.

Conclusion

The HDFC Bank SWOT analysis reveals that the bank stands tall as India’s financial leader, thanks to its strong network, digital innovations, and high customer satisfaction. However, weaknesses like limited rural penetration and dependency on the Indian economy remain.

Opportunities lie in global expansion, wealth management, and digital banking, while threats include rising NPAs, fintech disruption, and cybersecurity challenges. The analysis of HDFC Bank makes it clear: adapting to technological changes and expanding its footprint will be key to sustaining leadership in 2025 and beyond.

FAQs

What is HDFC best known for?

HDFC is best known for its leadership in retail banking, housing finance, and digital banking innovations.

How does HDFC Bank compare to ICICI Bank?

While ICICI is more aggressive in marketing and corporate lending, HDFC leads in retail banking and payment technologies.

What impact has the HDFC–HDFC Ltd. merger had?

The merger has created India’s largest financial powerhouse by combining retail banking strength with a massive home loan portfolio.

What are the biggest challenges for HDFC Bank in 2025?

Challenges include rural penetration, rising NPAs, increasing fintech competition, and the need for stronger cybersecurity.

Why is SWOT analysis of HDFC important?

It helps understand the bank’s strengths, weaknesses, opportunities, and threats, giving insights to investors, students, and policymakers about its current and future position.

A digital marketer with a strong focus on SEO, content creation, and AI tools. Creates helpful, easy-to-understand content that connects with readers and ranks well on search engines. Loves using smart tools to save time, improve content quality, and grow online reach.